Last week, I dropped a cheque into the litter bin (yes, litter bin) of the bank’s auto lobby instead of the cheque deposit box. The hotline personnel said they would help to retrieve my cheque, but I needed to wait 5 working days for any update. In the meantime, I might lose $1,000+ if someone picked up my cheque and knew how to bank it into another account or encash it.

Have you lost or misplaced a cheque before?

Your risk depends on how you write your cheque.

Have you lost or misplaced a cheque before?

Your risk depends on how you write your cheque.

Do you know that cheques for company credit card expenses can be used to pay for personal credit cards instead? Fraudsters have also siphoned off money by depositing cheques that were not bearer-crossed into their own bank accounts.

These real cases did not involve any forgery, so they could be prevented by handling and writing cheques better.

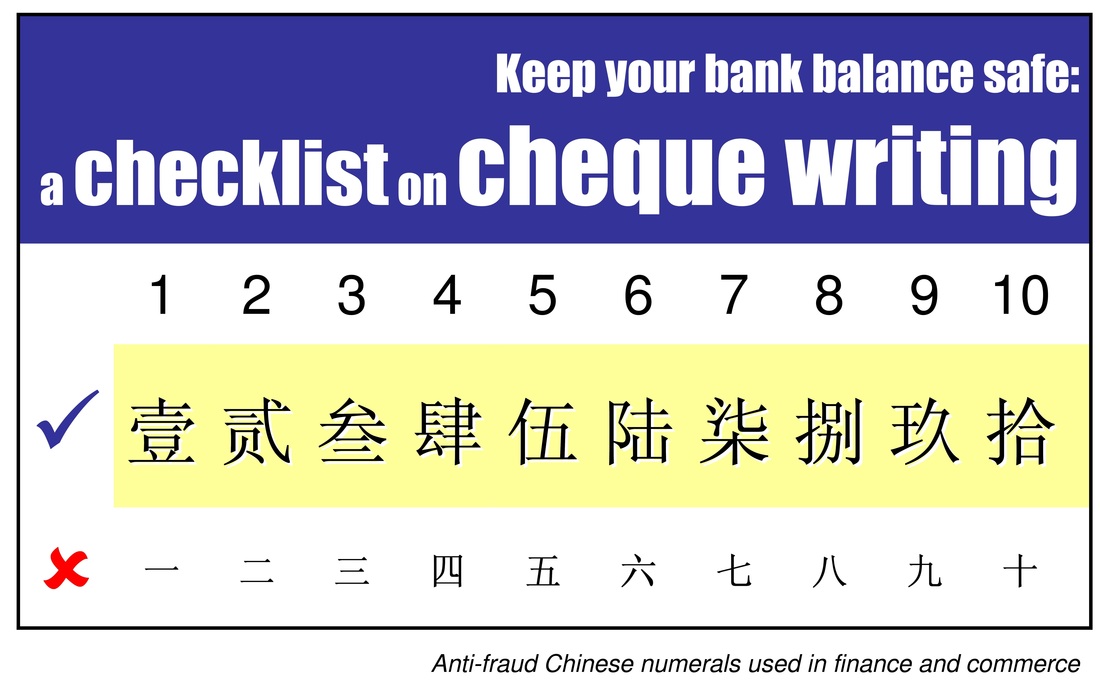

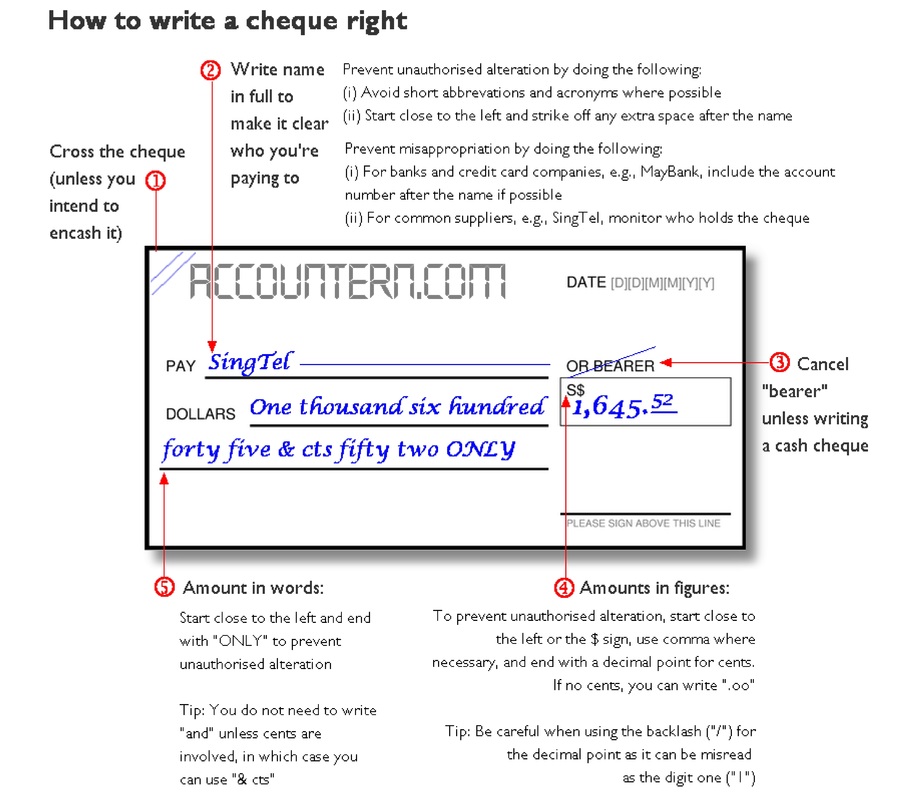

If you want to sleep better at night, look after the following five areas when you write your next cheque.

These real cases did not involve any forgery, so they could be prevented by handling and writing cheques better.

If you want to sleep better at night, look after the following five areas when you write your next cheque.

What is a "not negotiable" crossing?

If you mark your cheque "not negotiable", you protect yourself against any third party claim should the cheque fall into the wrong hands.

To understand non-negotiable, we need to start with negotiable instruments.

A cheque is a promise to pay from a bank account. In banking practice, a cheque is a type of negotiable instruments. A negotiable instrument is used in trade because it replaces cash and yet has two benefits of cash: transferable and negotiable.

Transferability means that a cheque can be passed from one person to another person for payment (through a process called endorsement). To understand transferability, think of cheques as cash equivalents.

Negotiability follows transferability, and means that as the cheque is passed along, the right of the transferee is not affected even if the transferor is later proved to be an illegal owner.

Just like cash. Suppose someone steals money from his neighbour and uses it to pay you for goods, you're entitled to keep the cash if you did not know those were ill-gotten gains. A cheque is similar: if someone steals a cheque and endorses it to pay you (never mind the process and whether the banks here allow it), you get to keep the cheque.

Now, when a cheque is marked "not negotiable", it means such: NOT negotiable. This means that the moment a non-rightful person gets hold of the cheque, it becomes invalid to all subsequent holders. The cheque has, from that moment, become like a counterfeit note. You can't use a counterfeit note to buy things, even if you yourself were cheated with it.

To understand non-negotiable, we need to start with negotiable instruments.

A cheque is a promise to pay from a bank account. In banking practice, a cheque is a type of negotiable instruments. A negotiable instrument is used in trade because it replaces cash and yet has two benefits of cash: transferable and negotiable.

Transferability means that a cheque can be passed from one person to another person for payment (through a process called endorsement). To understand transferability, think of cheques as cash equivalents.

Negotiability follows transferability, and means that as the cheque is passed along, the right of the transferee is not affected even if the transferor is later proved to be an illegal owner.

Just like cash. Suppose someone steals money from his neighbour and uses it to pay you for goods, you're entitled to keep the cash if you did not know those were ill-gotten gains. A cheque is similar: if someone steals a cheque and endorses it to pay you (never mind the process and whether the banks here allow it), you get to keep the cheque.

Now, when a cheque is marked "not negotiable", it means such: NOT negotiable. This means that the moment a non-rightful person gets hold of the cheque, it becomes invalid to all subsequent holders. The cheque has, from that moment, become like a counterfeit note. You can't use a counterfeit note to buy things, even if you yourself were cheated with it.

What then is an "account payee" crossing?

With this knowledge of non-negotiability, you can now progress to understand "account payee" crossing.

The "payee" is the name of the person written on the cheque after the word "Pay...".

When you cross a cheque "account payee", you're saying:

"Dear Collecting Bank, do you see the name of the person written on this cheque? Yes, I intended for the money to go into this person's account only. If you're representing any other person to collect this cheque, you’re responsible to make sure that the cheque has been legally transferred to that person."

Therefore, an "account payee" crossing also protects you from fraud and irregularity. In fact, it is more restrictive than a "not negotiable" crossing, such that the later is not necessary for a cheque already crossed “account payee”.

The "payee" is the name of the person written on the cheque after the word "Pay...".

When you cross a cheque "account payee", you're saying:

"Dear Collecting Bank, do you see the name of the person written on this cheque? Yes, I intended for the money to go into this person's account only. If you're representing any other person to collect this cheque, you’re responsible to make sure that the cheque has been legally transferred to that person."

Therefore, an "account payee" crossing also protects you from fraud and irregularity. In fact, it is more restrictive than a "not negotiable" crossing, such that the later is not necessary for a cheque already crossed “account payee”.

Why do people cross cheques both "not negotiable" and "account payee"?

The reason: play safe.

Another practical reason: If you buy a self-inking stamp, the one with both the "not negotiable" and "account payee" crossings costs the same as the stamp for only one crossing (i.e., either "not negotiable" or "account payee"). So most people get the stamp with both crossings.

Another practical reason: If you buy a self-inking stamp, the one with both the "not negotiable" and "account payee" crossings costs the same as the stamp for only one crossing (i.e., either "not negotiable" or "account payee"). So most people get the stamp with both crossings.

Your action

Regarding the cheque that I dropped into the litter bin of the ATM auto lobby? I did not bother to stop the cheque because I knew it was a safe cheque.

Therefore...

The next time you write a cheque, follow the five-point checklist above. (Tip: get a franking machine).

Or when you receive one, especially for big amounts, do the following if the drawer did not do any of these:

Therefore...

The next time you write a cheque, follow the five-point checklist above. (Tip: get a franking machine).

Or when you receive one, especially for big amounts, do the following if the drawer did not do any of these:

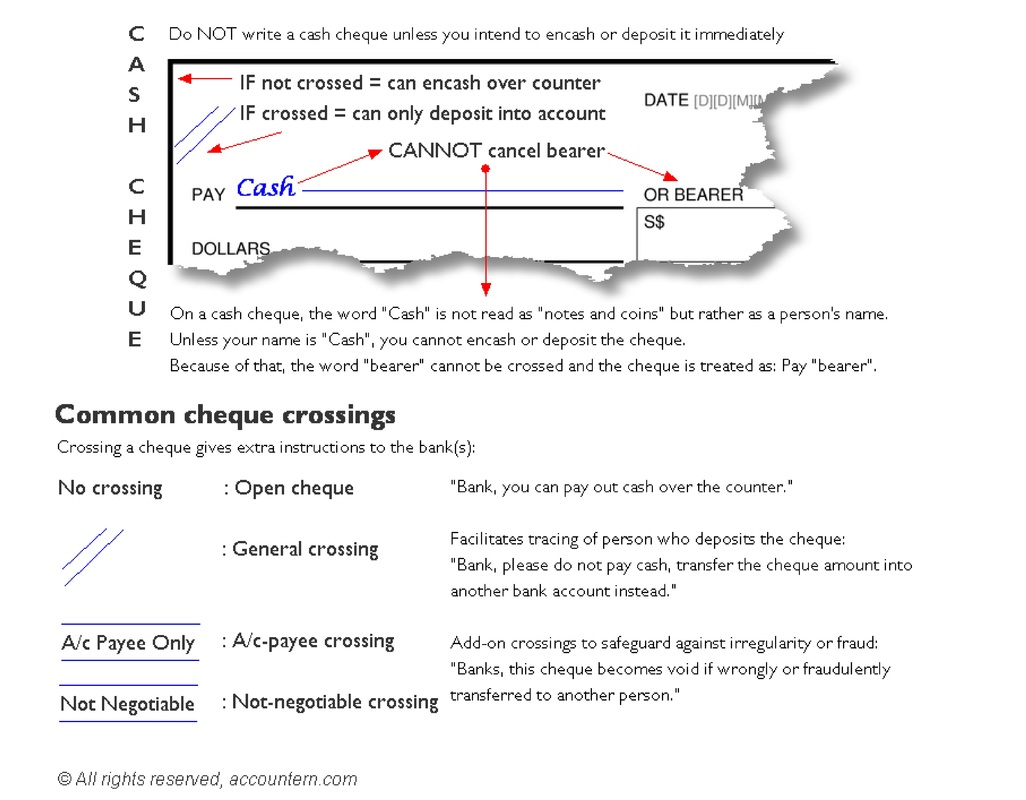

- Cross the cheque "account payee" (tip: buy a self-inking stamp)

- Cancel the word "bearer" (unless it is a cash cheque)

- Strike off any empty space after your name